Are you considering an EV to make an environmental impact? If so, there are some factors to think through before you can proclaim yourself “emission-free”.

To be or not to be, that is the question. A binary choice. In the past, a SURS Self-Managed Plan (SMP) participant once had a binary choice like this. Annuitize or not annuitize. Annuitization would ensure a lifetime stream of income and the retiree health insurance. By not annuitizing, or taking the lump sum option, one was turning down the health insurance and assuming the risk of portfolio management.

Along with the rebranding of the SMP to the SURS Retirement Savings Plan (RSP), more choices were added. With more choices comes more complexity. Participants may still choose to annuitize the lump sum as they have in the past. Alternatively, one may choose to use the new Secure Income Portfolio (SIP). Some of the new benefits SIP affords are:

1) the potential to have one’s retirement income stream increase with market returns, and

2) the ability to leave the residual value of one’s SURS account to heirs at death.

Along with these new choices come more options. One new choice is the ability to only use half of the account to produce guaranteed income and still maintain state-provided health insurance. This ability provides guaranteed income through the Secure Income Portfolio (“SIP”). The remaining 50% would be kept in the Lifetime Income Strategy (“LIS”) and can be accessed as needed.

To review a more comprehensive explanation and analysis of the new RSP, you can download a whitepaper we authored here.

As we have begun to assist clients through the retirement process since the change from SMP to the new RSP Plan, here are a few items we have learned along the way.

There are different rules for participants retiring before age 60 when using the SIP.

If you choose to have some balance remain in LIS and not be subject to the guaranteed payout through the SIP, you can’t access the amount in the LIS until you turn age 60. One benefit of using the SIP is that you can choose to only use half the account for generating pension income and still qualify for the health insurance benefit. After age 60, the other half – the LIS half – can be used or withdrawn as desired. However, prior to age 60 that freedom to withdraw the account does not apply.

If you retire before age 60, your SIP benefit cannot yet increase with market increases – it is “locked” until age 60. Just like at age 60 and later retirement, the benefit amount may not go down. The “floor” is set at retirement. Once one reaches age 60, benefit increases due to market gains can be granted. If market decreases do happen between retirement and age 60, the principle in the LIS account is reduced even though the benefit is not.

The benefit of using the SIP includes:

• ability to allocate a portion of your account balance to draw upon at your discretion

• ability to leave the leftover balance of your account to a beneficiary and heirs at death

• ability for guaranteed income to increase overtime with the performance of investments

However, these benefits come with an expense – you could potentially receive a smaller pension relative to other options.

The pension amount can be expressed as a withdrawal rate, which is the annual benefit divided by the total lump sum balance. For example, a pension benefit of $5,000 per month or $60,000 per year on a $1 million account balance equates to a withdrawal rate of 6%. When activating the SIP, or annuitizing your balance, rates will depend on a variety of factors including, but not limited to: age, whether a survivor benefit is being provided, and market rates at retirement.

Under recent rates, if one is age 65 with no survivor benefit and annuitizes the account (without using the SIP), a withdrawal rate of 7.4% could be expected.¹ If the same individual uses the SIP they could expect a withdrawal rate of 4.81%.² In real dollar terms in this example, with a $1,000,000 balance, it would mean the difference between receiving $6,183 per month and $4,008 per month.

In this example, the monthly pension benefit is only 65% of what it might have been had the account been fully annuitized. One might think “I worked hard all these years and this is all I get?” Keep in mind, you are giving up some monthly benefit in order to potentially get future rate increases, and to preserve that value for heirs.

While most assets were transferred to Voya during the changeover to RSP, some legacy funds may still exist at TIAA or Fidelity. At retirement, remaining balances in TIAA or Fidelity need to be annuitized with that company or transferred to Voya and incorporated into the SIP. One of these two actions are mandatory to qualify for and enroll in the SURS health insurance benefit. This would apply even if the TIAA balance is extremely small and would not produce much monthly income.

Once your lifetime benefit in the LIS Secure Income Portfolio is “activated,”³ there’s no going back. One cannot later terminate the contract and take the entire LIS and SIP balance for one’s own. This might apply if you are an early retiree (before Medicare age 65) and need the SURS health insurance. Before 65 the health benefit is large but diminishes following enrollment in Medicare. At 65, if you were to want to terminate enrollment, and take the lump sum balances for one’s own management and quit paying the higher fees for benefits you’re no longer using, the rules would prevent enacting this strategy.

[1] Principal Life Insurance Company Illustrative Table of Annuity Premiums for SURS Rates as of October 1, 2022

[2] Chart – SURS Blended Rates- Rolling Periods, Lifetime Income Strategy – Q4 2022

[3] SURS Retirement Savings Plan Member Guide, page 22, https://surs.org/wp-content/uploads/Guide-RSP.pdf

We have found that retiree health insurance benefits can be the most common point of confusion for State of Illinois employees retiring under the State University Retirement System (SURS). In this post, we will break down the basics of the Retiree Health Insurance Benefit, how to qualify, and the features and drawbacks of this benefit.

Special Note for SURS Retirement Savings Plan participants: In fall of 2020, SURS rolled out the newly rebranded SURS Retirement Savings Plan (RSP), which has added another layer of complexity. See the whitepaper we wrote for a more detailed overview of this change.

To begin, let’s discuss the qualifications for retiree health insurance benefits. The first requirement is service credit. Service credit can vary based on your SURS membership Tier, which is determined by the date of first employment under a SURS covered employer. For anyone with service credit prior to January 1, 2011, you are considered a Tier I participant. A Tier I participant is eligible for retiree insurance benefits after 5 years of service credit. Anyone beginning service credit on or after January 1, 2011 is a Tier II participant. 10 years of service credit is required for Tier II participants to be eligible for any retiree health insurance benefit.

The service credit discussed above is the minimum requirements to be eligible for retiree health insurance. Meeting the minimum service credit requirements only provides for a subsidy of the cost of this benefit. To have your insurance fully subsidized by the State of Illinois, you need 20 years of service credit. Members who meet the minimum coverage requirements and have less than 20 years split the cost of coverage with the state. The chart below summarizes this cost split:

Costs above are for the employee only. Coverage for a spouse or dependents is available for an additional cost.

The second requirement in addition to meeting the service credit requirements to qualify for retiree health insurance is to annuitize your pension. If you separate from service and defer taking a monthly retirement benefit under SURS, you would not be entitled to the retiree insurance benefit until you have annuitized your pension plan. Taking a refund of your pension plan balance, including rolling over your plan balance to an IRA or other retirement plan will result in a forfeiture of retiree health insurance benefits.

Annuitization of SURS is the process of converting your benefit into a stream of income payable monthly for the remainder of your life. For the Traditional and Portable plan, this is fairly straightforward. Your pension is based the higher of two formulas which SURS will calculate for you. Your main decision is whether to select a survivor benefit for your spouse or a qualified dependent.

The Retirement Savings Plan has more flexibility, which makes annuitizing a bit more complex. Here is a summary of your options.

1. Annuitize the entire balance of your SURS RSP. This annuity will generally be administered for SURS through Principal Insurance company, or at TIAA if you still have funds in your RSP portfolio invested at TIAA.

2. Move at least 50% of your RSP portfolio balance into the SURS Secure Income Portfolio and activate the lifetime income benefit. When selecting this option, all RSP investment funds not otherwise annuitized must be first moved into the Lifetime Income Strategy (LIS) portfolio. Next, with all non-annuitized RSP funds in the LIS portfolio, at least 50% of those LIS funds must then be moved into the SIP with its guaranteed income benefit. After moving all funds into the LIS and activation of at least 50% of your LIS fund total into the guaranteed SIP, any LIS funds not in the SIP may be moved back to RSP Core Funds or withdrawn.

3. A combination of Options 1 & 2 – for example, you could use 1/3rd of your RSP account to buy an annuity through Principal. With the remaining RSP balance, allocate 50% to the SIP for lifetime income and 50% to the LIS or Core Funds for periodic withdrawal.

We have commonly heard the misconception that RSP participants must use the new SIP to maintain health insurance, which is not true. Electing an annuity remains an option.

It is possible to retire from the University and delay drawing your pension. This may be beneficial if you have alternative insurance coverage through new employment or a spouse. Deferring your benefit has two potential benefits. First of all, your pension benefit (traditional or portable) may increase or the balance of your account can continue to grow (RSP). Secondly, if you are not yet Medicare-eligible, the State of Illinois will pay an additional monthly incentive to opt out of retiree insurance.

A University Employee has 20 years of service at age 50, at which point she leaves university employment to pursue a second career with a private sector employer. The new employer offers health insurance. The employee leaves her account balance with the SURS RSP, which allows the balance to continue to grow. At age 63, she fully retires from her private sector position and needs health insurance. At this point, she activates one of the RSP income options to qualify for health insurance as a State of Illinois retiree.

There may be cases where an individual chooses to forgo their SURS retiree health insurance benefits, but before making this irrevocable decision, it is important to understand what those health insurance benefits are worth.

Those in the SURS RSP are also required to participate in Medicare. While working, everyone pays into the Medicare system. Upon turning age 65, you must sign up for Medicare. If you are still working and covered by your University insurance, you only need to enroll in Medicare Part A, but may delay Part B until you retire.

Medicare has three parts:

Part A, which covers Hospital services and is generally free for those age 65+

Part B, which covers doctor visits and other outpatient services. Part B has a monthly premium starting at $170.10 (2022); cost can increase based on income.

Part D, which covers prescription drug costs

Once you retire and become a SURS annuitant aged 65 or older, you are required to enroll in the Total Retiree Advantage Illinois (TRAIL) plan, managed through Illinois Central Management Services (CMS). This is a Medicare Advantage plan, which means it combines Medicare Part A, Part B, Part D and a Medicare Supplemental Policy (commonly known as a Medigap policy). Even under the TRAIL program, you still must pay the Medicare Part B premiums on your own. The State of Illinois subsidizes (or entirely covers) the rest of your supplemental health cost.

For a retiree with 20 or more years of service, age 65 or older and on Medicare, the value of this benefit is around $150 per month. This is based on the amount the State of Illinois covers for the cost of the Advantage Plan (Illinois Central Management Services, 2022).

For a retiree with 20 or more years of service and under the age of 65, the SURS health insurance benefit is significantly more valuable. Prior to Medicare eligibility, the State picks up the entire cost of their health insurance. For those retiring before age 65, the cost of health insurance can be a significant obstacle. For example, marketplace plans at healthcare.gov range in cost from $1,165 to $1,791 for a 60 year old male in the Champaign County area.

Health Insurance is one of the biggest obstacles we see for clients who wish to retire prior to eligibility for Medicare at age 65. If you are retiring early from the University, it could be a valuable benefit. The requirement to annuitize is the biggest obstacle, especially for those in the SURS Retirement Savings Plan. Once you are Medicare eligible, the value of the insurance benefit is less valuable as Medicare covers a significant portion medical expenses and Medicare supplement policies are low in cost as compared to private health insurance.

We have heard from many of our clients regarding concerns over the change in Insurance Providers for State of Illinois Medicare-Eligible Retirees. With so many clients impacted by this change, we have been following the news. Here is what we know so far and what we are recommending.

Starting with what we know, it is not much. We wrote up a short piece on our website on this a few weeks back, which you can read here. The major concern at this time is that Carle has not come to an agreement with the Advantage Plan Provider, Aetna. This means that Carle providers and facilities are not in-network for the new plan effective January 1, 2023. While the new plan is a PPO and should allow you to see out-of-network doctors, these services may not be covered if the provider is unwilling to bill through Aetna.

As far as we can tell, conversations between Carle and Aetna are ongoing and there is a possibility that an agreement will be reached before the new plan year. This would not be unprecedented. A similar process unfolded about 10 years ago when Health Alliance was dropped in favor of UnitedHealthcare. Recent comments from Carle and Aetna representatives may be more attempts to rally public pressure for negotiations than statements of actual status of negotiations.

The unfortunate part is this leaves a lot of uncertainty for current plan participants. Here is what we are recommending:

If you are currently undergoing treatment for chronic or critical medical issues and absolutely cannot switch doctors, be prepared to switch to a private policy:

November 30th – Deadline to opt out of the TRAIL / State of Illinois Medicare Plan

December 7th – Deadline for Medicare Open Enrollment to select your own private plan

Research Alternative Plans - Medicare's Website is the best resource as you can narrow in to providers covered in your area.

Private policies generally run $50-175/month/person, but can be higher or lower depending on deductible, co-pays, etc.

Inputting your current prescriptions will provide you a better total out of pocket cost estimate.

Pay attention to vision and dental coverage.

For everyone else, it is probably best to take a wait-and-see approach. If Carle and Aetna reach an eleventh hour agreement, you avoid all the hassle of unenrolling and reenrolling from TRAIL next year. If they do not reach an agreement, you could also unenroll from TRAIL during the next enrollment period near the end of 2023.

In September, the State of Illinois Department of Central Management Services (CMS) announced changes to the State of Illinois Retiree Insurance Program. These changes impact retirees enrolled in the Total Retiree Advantage Illinois (TRAIL) who are also Medicare Eligible. This applies to members who are currently enrolled, or plan to enroll in the TRAIL Medicare Advantage Prescription Drug (MAPD) plan effective for the 2023 plan year.

Following a proposal process, the State of Illinois has selected Aetna Medicare Advantage Prescription Drug (MAPD) PPO Plan as the new medical and prescription drug plan beginning January 1, 2023. This will replace the existing plans, most commonly the HMO Plans through UnitedHealthcare, Health Alliance, or Humana. This change is automatic and does not require participants to take any action .

Here are a few Frequently Asked Questions (FAQs) that may help you:

The contract with current providers expires December 31, 2022. State law requires a competitive process to compare proposals submitted by various vendors. Aetna was selected as part of this process.

With any change in insurance provider also comes concern over coverage of existing doctors and hospitals. While it is yet to be seen how these concerns will be addressed, it is worth noting this is not a new process. A similar process unfolded when Health Alliance was dropped in exchange for UnitedHealthcare.

No. To maintain coverage under the Total Retiree Advantage Illinois (TRAIL), including subsidized premiums under your retirement annuity, you and your dependents will automatically change to the new provider.

You may opt of out of TRAIL by visiting MyBenefits.illinois.gov. This must be completed by November 30, 2022. If you opt out, you will want to select a new Medicare Supplement and Part D or Medicare Advantage plan in the private market. You will be responsible for the full premiums for these Supplement/Advantage plans. You can compare plans at Medicare's Website. If you opt out, you may re-enroll in the TRAIL program with a qualified life event or during the next year’s open enrollment.

This change only impacts members and their dependents whose coverage is under a Medicare Advantage plan. If you or any dependents are not Medicare-eligible, your coverage is through the State Employees Group Insurance Program (SEGIP) and is not impacted by this change. This change may impact you if you become Medicare eligible in the future.

Medicare is commonly made up of three parts:

Part A – Covers Hospital Services

Part B – Medical Insurance

Part D – Prescription Drugs

Most Medicare participants also add a Medicare Supplement plan to cover any gaps and add services above the base Medicare plans.

Medicare Advantage Plans combine all the above plans into a single plan, administered through a private health insurance company. In this case, Aetna is the private company who will take over administration.

Yes. While a Medicare Advantage plan replaces original Medicare, you are still responsible for Medicare Part B premiums, which are either paid directly to Medicare or deducted from Social Security benefits. Note that, for most people, Medicare Part A is free (paid through Payroll taxes while working). Your Part B premium is based on your income and can change from year to year. Part D may also have a supplemental cost. These premium adjustments are called the Income Related Monthly Adjustment Amounts (IRMAA) as follows:

As mentioned previously, for those opting out, actions will need to be taken. For those choosing to stay on the TRAIL MAPD program, the change is automatic for members and their dependents. You will receive a welcome kit in the mail from Aetna with more information on the plan and new member ID Cards. With all the Medicare spam mail that gets sent out, keep a sharp eye out for any correspondence from AETNA, CMS, or anything with the TRAIL logo.

SURS News Release Retiree Healthcare Update - SURS

Illinois Central Management Services My Benefits Website

Aetna Coverage Details State of Illinois | Aetna Medicare

Medicare Premiums Detail at Social Security - IRMAA Sliding Scale Tables

TRAIL Enrollment Guide (2022) FY 2022 Benefit Choice

Selecting the right Pension Plan under SURS is complex. Below are some of the factors we discuss and a summary of how they may impact your decision:

|

|

Traditional Plan |

Portable Plan |

Retirement Savings Plan |

|

High-income Participants |

Less Favorable |

Less Favorable |

More Favorable |

|

Participant Control of Investments |

No |

No |

Yes |

|

Pension Income Guaranteed |

Yes |

Yes |

No |

|

Career Stage |

Favors Late-Career |

Favors Late-Career |

Favors Early-Career |

|

Flexible Options at Retirement |

Least |

Moderate |

Most |

Congratulations on your new role with an Illinois public institution! In addition to meeting your new colleagues, learning the ropes of your new department, and developing your new courses (if instructing), you will need to select a pension plan under the options offered through the State Universities Retirement System (SURS). Choosing the right plan can be complex, so we have narrowed down the factors we have found make the biggest difference.

We encourage you to be diligent in your selection process, but do not delay! While you have 6 months to select a plan, matching contributions are not allocated to the self-directed plan until you decide. If you fail to decide, you will automatically be enrolled into the default option of the Traditional Plan.

So, let’s get started!

When you begin employment, you must select from three plan offerings: Traditional, Portable, or Retirement Savings Plan (hereafter referred to as RSP). The RSP was previously known as the Self-Managed Plan (SMP) until it was updated and rebranded in 2021. You may find that some colleagues still refer to it as such.

While all three plans are considered pension plans, they can be distinguished at a high level between defined benefit and defined contribution plans. In a defined benefit pension plan, your retirement income is based on a formula. The Traditional and Portable plans fall under this category. In this case, your income at retirement is determined by your average earnings and length of service. The pool of money that backs this pension is managed by SURS and the investment risk is borne by the State of Illinois.

In contrast, the RSP is a defined contribution plan. Your future retirement income is based on the balance of your account at retirement. Your contributions along with matching contributions from the state are deposited into a separate account for your benefit. You are responsible for selecting and managing the investments in that account and bear the investment risk of that account. When you retire, you can convert that account balance into a stream of income called an annuity. The level of this benefit will be determined by the balance of your account at retirement. You can read about these annuity options in the white paper we wrote about this plan by clicking here.

|

Options |

Plan Type |

Summary |

|

Traditional Plan Portable Plan |

Defined Benefit |

Retirement benefit based on formula Employer bears investment risk |

|

Retirement Savings Plan |

Defined Contribution |

Retirement benefit based on account balance

You bear investment responsibility and risk |

One major difference in the plans is the level of income counted towards your pension benefits. Due to this difference, salary and future growth potential could be the single biggest factors to consider in selecting your plan.

The Traditional and Portable plans are limited to a state-determined Maximum Pensionable Earnings, currently $116,470.42 (Fiscal Year 2022). If your salary exceeds this limit, your contributions to the plan (8% of salary) and employer matching contributions (7.6% of salary) will only be based on your wages up to the limit. Similarly, your final average salary to determine your annual pension will be capped based upon this same limit.

The RSP uses a federal limit for Maximum Pensionable Earnings, currently $290,000 (Fiscal Year 2022). This makes the RSP more favorable to those whose current or future salary may exceed the annual Traditional and Portable annual wage limit. To illustrate, consider the following examples.

Dr. Zhao has been recruited by the University of Illinois as a Professor and a starting salary $200,000 per year. She selects the SURS Traditional Plan. She works for 25 years, retiring at age 67. Her pension is $64,000/year[i] or $5,333/month.

Let’s assume the same base facts as example 1, except Dr. Zhao selects the RSP plan. She invests her RSP Account Balance into a portfolio of 40% Bonds and 60% Stocks, earning an annualized return of 9.4% per year[ii]. At age 67, she retires with a SURS RSP Balance of $2.8 million. She then annuitizes this balance and receives a lifetime income stream of $142,000/year or $11,833/month[iii].

There is a crucial difference between Examples 1 and 2. As an employee, your contribution to SURS ends after your income exceeds the Maximum Pensionable Earnings. Consider the following table to illustrate:

|

Plan |

Maximum Pensionable Earnings |

Contributions Assuming $200,000 Salary |

|

Traditional Plan Portable Plan |

$116,470.42 |

Employer: amount required annually based on actuarial formula

Employee: $116,470.42 x 8% = $9,317.63 |

|

Retirement Savings Plan |

$290,000.00 |

Employer: $200,000 x 7.6% = $15,200

Employee: $200,000 x 8% = $16,000 |

This means Dr. Zhao would contribute over $6,682.37 ($16,000 - 9,317.63) more per year to the SURS RSP than the SURS Traditional Plan.

Assume the same facts as Example 1, except Dr. Zhao chooses to add the $6,682.37/year to a supplemental retirement savings plan (403b). We will also assume the same hypothetical portfolio used in Example 2. At the end of 25 years, she has an account balance of about $600,000. Assuming the same annuity rates as Example 2, she could receive an estimated additional income of $30,000/year, or $2,500/month, from her 403b account.

Together, these three examples illustrate the impact the salary cap has on the outcome. For someone whose income exceeds the salary cap, selecting the Traditional or Portable plan results in the missed opportunity to receive matching contributions.

For those who choose the RSP, one feature of the plan is the ability to control investment decisions. Voya is the current plan custodian. Through their platform you can allocate your account balance between a mix of different investment choices. One option is to select a custom mix of Core Funds. Core Funds are a set of low-cost, index funds designed to track a variety of investment benchmarks. Participants can choose a custom combination of Core Funds in proportions that they deem most appropriate for their situation, but are self-responsible for managing the balances between the Core Funds over time. An alternative to the Core Funds is the Lifetime Income Strategy (LIS) Fund. The LIS is an investment fund that is managed to automatically adjust the risk level of the fund based on your planned retirement date.

As illustrated in the above examples, choosing the RSP provides participants with the potential for maximizing pension payments in retirement. However, the downside is that you also bear the investment risk that comes along with your investment selections, which, depending on market and investment performance, can directly impact the future balance of the RSP and thus, the size of the pension payments which can be generated by that RSP balance.

If you prefer to have the employer retain the investment risk and receive a guaranteed income, then the Traditional or Portable may be a more suitable option. These plans are professionally managed by the investment staff with SURS. No matter the outcome of investment performance, your ultimate pension benefit is guaranteed.

While investment returns in the future cannot be predicted based on past performance, historical data generally shows more favorable returns for those who are invested for a long period of time[iv]. This suggests someone entering employment earlier in their career could benefit from a long period of time to allow investments to compound and grow in value, which may favor the Retirement Savings Plan.

Someone nearing the end of their career may not have a long-time horizon to ride out the ups and down of investment performance. In that case, a new employee in their later working years may favor enrolling in the Traditional or Portable plan.

The trend has been toward a more mobile workforce, where multiple job changes throughout one’s career are not uncommon. Academia is not immune to this trend. Therefore, you should consider the flexibility and portability of benefits in the event of an employment change. Here is a summary:

The Traditional plan has the least flexibility for departure or refund.

Requires 10-years of service credit to vest.

If you are fully vested and leave SURS-covered employment, you can:

Wait and draw benefits at full retirement age, or

Take a refund of your own contributions plus interest. Employer matching contributions are forfeited with this choice.

If you are not yet vested and leave SURS-covered employment, you are only entitled to a refund of your own contributions. Employer contributions are forfeited unless you later vest.

The Portable plan offers some benefits of the defined-benefit plan while maintaining some flexibility in case of departure.

Requires 10-years of service credit to vest.

If you are fully vested and leave SURS-covered employment, you can:

Wait and draw benefits at full retirement age, or

Take a refund of your contributions, employer matching contributions, plus interest.

If you are not yet vested and leave SURS-covered employment, you are only entitled to a refund of your own contributions. Employer contributions and interest are also refundable after 5 years of service credit.

The Retirement Savings Plan offers the most flexibility.

You vest with 5 years of service credit.

If you are fully vested and leave SURS-covered employment, you can take a refund of your contributions, the employer contributions, and growth and interest of the account.

If you are not fully vested and leave SURS-covered employment, you can take a refund of your contributions and growth and interest of the account. Employer contributions are forfeited.

For all plans, eligibility for retiree health insurance requires you to fully vest. Taking the full refund option for any pension will forfeit retiree health insurance benefits.

In exchange for reduced flexibility, the Traditional plan offers the most generous survivor benefits. Survivors would receive 2/3rds of your accrued monthly retirement benefit, payable to your eligible survivor. This benefit comes at no extra cost to you.

Following the same facts as example 1, assume that Dr. Zhao had selected the SURS Traditional pension with a base benefit of $5,333/month. If she were to die shortly after retiring, her spouse would be entitled to a survivor benefit of $3,555/month for life. At the death of Dr. Zhao and her spouse, no additional survivor benefits would be payable to children or other heirs.

The Portable plan only offers a default survivor benefit if you die before reaching retirement. In that case, the benefit is 50% of your accrued retirement benefit (as compared to 2/3rds under the Traditional plan). Upon retirement, you can choose to purchase a survivor benefit greater than 50% at a cost to you of reduced lifetime payments.

Following the same facts as example 1, assume that Dr. Zhao had selected the SURS Portable pension with a base benefit of $5,333/month. If she were to die shortly after retiring, her spouse would not be entitled to any survivor benefit. At retirement, Dr. Zhao could instead choose to take a reduced monthly pension to add a survivor benefit for 50%, 75% or 100% of the original pension.

The RSP does not provide an automatic lifetime survivor payment. You or your survivor are always eligible for a refund of your own contributions and earnings. After 1.5 years of service, employer matching and related earnings are also refundable to survivors. Your survivor may choose a lifetime payment with this refund, with the amount of such payment based on your account balance at that time.

This guide was written for those enrolling in SURS now and are therefore in Tier II SURS plans. This applies to those enrolled on or after January 1, 2011. If you first enrolled in SURS prior to this date and are a Tier I participant, some of these plan provisions may be different.

I’ll note that many clients consider the RSP a refuge from the troubled finances of the State of Illinois. The idea is that funds are held separately, in-trust, and therefore safe from the creditors of the State. This is true. By federal law, RSP funds must be deposited in a timely manner to your account, including employer matching. State matching of the other pension plans has not always been made timely, which is a big part of the pension underfunding problem.

However, this advantage of the RSP does not make the Traditional or Portable plans “unsafe”. The Illinois constitution states that pension benefits cannot be diminished, which guarantees participants their right to future benefits. Previous attempts at pension reform have tested and found this guarantee to be true. Unlike municipalities and territories, Detroit and Puerto Rico being recent examples, a State may not go bankrupt and therefore discharge the indebtedness of pension through bankruptcy. While it is yet to be seen how the state will solve its current financial crisis, it must pay the promised bill of pensions.

Regardless of whichever plan you choose, I would also encourage you to fund additional savings beyond your mandatory pension contributions. While the SURS system does provide generous pension benefits, the pension was not designed to cover all your needs beyond working years. Additionally, depending on your work history, you may not qualify for social security benefits as you do not participate in the social security system while actively participating in SURS. Even if you have a past earnings history in social security, your social security benefits may be reduced as a result of the benefits you earned while participating in SURS. While there are many savings options out there, the 403b and 457 savings plans offered through the University are often a good place to start. We generally recommend supplemental savings of at least 7% and ideally 10% of earnings beyond your required SURS contributions.

Navigating this initial decision on retirement plan choice will have a lasting impact on your future financial security. Compounding the importance of this decision, it must be made in the flurry of other important activities of moving, starting a new job, selecting other benefits and adapting to your new role. If you need help interpreting these decisions in your own financial life or want the peace of mind that you have considered the entire picture, please let us know. Many of our clients are members or retirees of SURS. We have helped hundreds of clients through the complexities of pension decisions. If you would like our perspective or professional opinion on your own decisions, Contact Us today!

SURS Traditional - SURS Traditional Guide

SURS Portable - SURS Portable Guide

SURS Retirement Savings Plan - SURS RSP Guide

[i] Calculated using the General Formula: 2.2% x 25 Years of Service x the maximum pensionable earnings limit of $116,470.42. Result rounded to the nearest thousand for simplicity of reading. There is a second formula called Money Purchase formula based on investment returns that may result in different pension calculation. We used the General Formula because your benefit can never be less than this result.

[ii] Investment Returns based on Shea, B. (2021). Investment Returns since 1926-2021 from Ibbotson's SBBI.

[iii] Future account balance calculated on investment return as described above and is not guaranteed. Past performance does not predict future results. Annuity calculated using a 50% Joint and Survivor Annuity Rates for 65-Year-Old Annuitant and 60-Year-Old Spouse as provided by Principal Life Insurance Company, Illustrative Table of Annuity Premiums for SURS Rates as of Jan. 1, 2021

[iv] How risk, reward & time are related (2022). Vanguard. Risk, reward & compounding | Vanguard

This post was updated August 2022.

In fall of 2020, the State University Retirement System (SURS) rolled out the newly rebranded SURS Retirement Savings Plan (RSP). A revamp of the existing SURS Self-Managed Plan, these changes extended beyond a new name to include a different plan administrator, new investment option lineup, and an additional income option for retirees. We have spent the last 6+ months diving into the details of the plan and writing the following paper to present our findings.

You may download the paper below.

Executive Summary:

It is clear from our research this new plan is extremely complicated. One of the biggest changes is SURS outsourcing a major component of the plan to a third-party company, Voya. In our experience, even the SURS call center employees are not fully trained on the inner workings of the new plan or its features. In some cases, we were referred to Voya representatives to answer questions.

The paper present education and details about the new plan as follows:

An overview of retiree health insurance benefits as a SURS retiree, including under the new RSP.

A detailed analysis of the new income option for the RSP, the Secure Income Plan.

A decision tree of factors that may influence whether to utilize the Secure Income Plan vs. an Annuity.

Commentary from us regarding this change and the rollout by SURS.

Disclosures

This was written to supplement the planning decisions we make with our ongoing clients in the context of a broader financial plan. We are providing this to the general public as educational materials. We would caution any reader that the SURS plan, including this new RSP, is very complex. We could not possibly cover every possible situation or consideration in this document. You should consult other advisors regarding tax, investment, and other financial implications before making an irrevocable decision. You should not rely solely on this document for any decisions regarding your SURS plan. While we believe the information in this report to be factual, we cannot guarantee it. We did cite sources whenever facts are presented. As representatives of SURS and/or Voya would not provide full details of plan features, the paper also describes when assumptions or estimates were used.

For members of the State University Retirement System (SURS) who are thinking of retiring soon, there are more changes coming to SURS starting in the summer of 2019. Under the most recent budget signed by Governor Rauner, Illinois law was amended to allow for two new options for retirees under SURS Traditional and Portable (Tier I). Those changes are:

Voluntary Automatic Annual Increase Lump Sum – Under this option, members can elect to forgo their 3% annual pension increase for a reduced 1.5% annual increase option. Under the 3% option, annual pension increases are compounded (increase by 3% original benefit plus increases). Under the 1.5% option, future benefits are increased by simple indexing (increase by 1.5% each year of the original benefit). The first increase will also further be delayed by the later of 1 year or age 67. If elected, members would receive a lump sum equal to 70% of the actuarial value difference of the 3% benefit and 1.5% reduced benefit.

Example: $50,000 annual pension, 3% default benefit vs. option 1.5% SIMPLE increase.

Note, total benefits after 31 years of benefit are:

· $2,500,134 for 3% option

· $1,898,750 for 1.5% option

When will this choice be available? SURS expects retirees to have this option for those retiring June 1, 2019 or later. It is possible the implementation will be delayed until July 1st. This option will be available until the earlier of June 30, 2021 or until appropriated funds are exhausted.

Who does this make sense for? Most members will be better off remaining with the 3% default option. While a large lump sum may be enticing, this option was only designed to replace 70% of the benefit you forgo. This may make sense if you have a lower than average life expectancy (such as a terminal or chronic illness).

Voluntary Pension Buyout for Vested, Inactive Members – This option would allow SURS (as well as SERS and TRS) members who are vested but no longer active to elect to receive 60% of the actuarial value of their future pension benefits as a lump sum. If elected, the recipient will still be entitled to health insurance benefits.

As with the changes to the cost of living, the availability of this option is expected to start in summer of 2019 and run until the earlier June 30, 2021 or when funds are exhausted.

Final Thoughts

Members should be very thoughtful and intentional before electing to forgo future benefits. Current, and likely large, lump sums of funds may be enticing. However, in many cases, you may give up much more than you get in return. We highly recommend seeking advice and counsel before you make a decision. Contact Us if you wish to learn more about our services and how we may be able to assist.

Finally, we wrote in our blog back in 2017 about SURS rolling out a new Tier III (aka – Hybrid Plan). After SURS analyzed the requirements under the law, it was determined it will not hold up to requirements set forth under Federal Law and therefore will not be moving forward. Without further action from the Illinois legislature, no changes are anticipated in the near future. It is worth noting that there is a possibility the newest Tier II (applicable to those hired on or after January 1, 2011) may also violate those same rules and require further compensation to participants to remain in effect. As a result, there remain many unknowns, and it may take years before a resolution regarding Tier II is finalized.

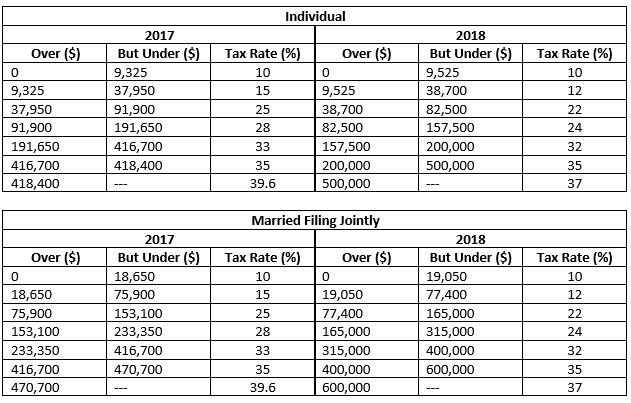

As you may have seen, the House and Senate have reconciled a final version of the Tax Cuts and Jobs Act of 2017 which President Trump signed into law this morning. While the bill has been signed it is important to note that additional time will be needed for full interpretation and adjustments as corrections and revisions are expected.

While a significant portion of tax changes relates to business organizations, many changes will affect individual taxpayers, as well. With such a major restructuring, it will likely take months for all of the changes to be ironed out.

Tax Brackets: The revised tax plan retains a 7 bracket tax system as proposed by the Senate. Most of the brackets enjoy a decreased rate, although the ranges of taxable income that define each bracket have been significantly adjusted. Below are the new tax rates compared to 2017. The table can be used to estimate how your tax rate may change in 2018.

Outcomes: It is nearly impossible to generalize who will see increases or decreases by this change alone. High-income couples will see some relief from the so called “marriage penalty”, up to $600,000 of taxable income. Otherwise, you will need to reference the following changes to fully gauge impact on your taxable income (impacting how these rate changes affect you). Many people will see lower overall rates, but loss of deductions may increase others overall tax liability.

Standard Deduction and Personal Exemptions: The standard deduction for all taxpayers has nearly doubled from $6,350 to $12,000 for individuals and from $12,700 to $24,000 for married couples. However, simultaneously is an elimination of personal exemptions of $4,050 per family member.

Outcome: An increased standard deduction will limit the benefit for many taxpayers to itemize deductions. Individuals and married couples with no kids and minimal itemized deductions may see a slight decrease in tax, while larger families may see higher tax due to the loss of personal exemptions. Keep in mind, changes to the Alternative Minimum Tax (AMT) may impact these changes for your situation.

Child Tax Credit: The Child Tax Credit is being expanded with an increase from $1,000 to $2,000 per qualifying child under 17. Also, the income phaseout levels are increased from $75,000 to $200,000 for individuals and $110,000 to $400,000 for married filing jointly. Additionally, a new credit of $500 has been added for qualified dependents that are not qualifying children (children 17 and older or non-child dependents such as parent).

Outcome: Intended to make up for the lost benefit of personal exemptions, individual results may vary based on family size, age of dependents, etc. Higher income taxpayers may benefit the most as they may have previously seen no benefit from personal exemptions due to AMT while now being eligible for the expanded Child Tax Credit.

Itemized Deductions

Mortgage Interest Deduction: For new mortgage contracts following December 15, 2017, the deductibility of interest on a primary residence will be limited to the first $750,000 of debt principal, as opposed to the current limit of $1,000,000. Interest deductibility on Home Equity Lines of Credit (HELOC) will be eliminated for existing and new loans when funds are not used to buy, build, or significantly improve the primary residence.

Outcome: Mortgage and HELOC interest remains a useful tax strategy for many taxpayers that will still be itemizing. We will simply need to be extra diligent about keeping record of how HELOC funds are used.

Charitable Contributions: While relatively unchanged, the limit for deducting cash donations to charities is being increased from 50% to 60% of Adjusted Gross Income.

Outcome: With the increased standard deduction, more individuals may see a benefit in “bunching” their charitable gifts on an every-other-year strategy.

State and Local Tax Deduction: Originally, both the Senate and the House looked to either eliminate or severely reduce these deductions. The final version of the bill allows both deductions but at a combined cap of $10,000. The cap is the same for both individual and married filing jointly returns. Furthermore, any pre-paid 2018 State income tax will not be allowed on 2017 tax returns.

Outcome: The cap on these deductions may limit the benefitting of itemizing deductions for some taxpayers, especially in the greater context of all the changes going into effect. Some people may benefit from pre-paying certain taxes before 12/31/2017. If you make estimated tax payments, you might benefit from pre-paying your 4th Quarter State estimated tax payment before the end of 2017. For those of you who live in a county that accepts prepayments for real estate taxes, you may also benefit from pre-paying your real estate taxes. Please note, many high-income taxpayers subject to AMT may not benefit the prepaying strategies. However, those same taxpayers will not also see a tax increase due to changes as their deductibility was already limited.

Medical Expense Deduction: Surprisingly, the medical expenses deduction will be temporarily expanded. For tax year 2018 and retroactively for 2017, the AGI threshold for this deduction will be reduced from 10% to 7.5%. An additional adjustment allows taxpayers affected by AMT to still enjoy the 7.5% threshold so that they can receive the benefit of this deduction, as well.

Outcome: Some taxpayers who previously thought their medical expenses were too low in 2017 for deducting might find they are in fact eligible. If you anticipate major expenses in 2017 or 2018, timing any other discretionary (deductible) medical spending into the same year may be beneficial.

Miscellaneous Itemized Deductions: All miscellaneous itemized deductions that were otherwise subject to the 2%-of-AGI floor have been eliminated. Some of the most common deductions that will be lost are as follows:

Outcome: In some cases, you may benefit from accelerating these deductions normally paid in 2018 by pre-paying by December 31st of this year. Note, this strategy may not apply to those subject to AMT in 2017.

Written by Karen Folk, CFP®, Ph.D., Founder & Advisor Emeritus of Bluestem Financial Advisors

Both my husband and I have been loyal clients of TIAA (formerly TIAA-CREF) for over thirty years. Throughout our academic careers, we chose TIAA over several possible providers. We were attracted to their low cost mutual funds and long nonprofit heritage of service to teachers. Founded in 1918 as the Teachers Insurance & Annuity Company to help teachers retire comfortably, they have become a leading retirement plan provider for academic, research, medical, cultural and government employees.

Recently, as an account holder, I have grown concerned by TIAA’s behavior towards us as consumers. We have noticed increasing encouragement by TIAA representatives to consolidate and rollover other retirement assets to their platform. We were notified in 2015 that TIAA had appointed a full-time representative locally. We were subsequently contacted on multiple occasions asking us to meet with this representative. After researching this individual on LinkedIn, I noted his past experience included sales roles with other large brokerage firms, but listed no Financial Planning credentials beyond the minimum required licenses.

A recent New York Times article “The Finger-Pointing at the Finance Firm TIAA” (October 21, 2017, Gretchen Morgenson), revealed some rather dramatic changes in TIAA that have led to whistleblower complaints to regulatory agencies as well as a lawsuit. The whistle-blower complaint filed with the Securities and Exchange Commission, obtained by The Times, “was filed by former TIAA employees who contend they were pressured to sell products that generated more revenue for the firm but were more costly to clients while adding little value”. This was followed by the NY Times article “TIAA Receives New York Subpoena on Sales Practices” (Nov 9, 2017). The NY state attorney general has subpoenaed records from TIAA to investigate possible regulatory infractions.

Both articles increased my concerns about whether the changes I noticed at TIAA are contrary to their long tradition of unbiased advice at low cost. As we investigated further, my husband was surprised to learn that parts of TIAA stopped being a nonprofit in 1997 – he, and I am sure many other TIAA clients, was not aware that much of TIAA is now a for-profit enterprise.

The NY Times October 21st article explains that, in 2005, TIAA established the Wealth Management Group. This group offers investment management services for a fee, a fee which is in addition to the underlying administrative and investment fees charged by TIAA funds. The lawsuit and whistleblower complaints claim that TIAA’s Wealth Management Group, now called “Individual Advisory Services”, is pushing customers into higher-cost products that generate higher fees. Given that TIAA continues to highlight its nonprofit heritage and its salaried employees, my concern is that TIAA clients are not aware of this conflict of interest.

Based on my own experience, experiences reported to us by clients, and the NY Times articles, we did some additional research we thought worth sharing.

We started by reading TIAA’s Form ADV, Part 2A, of the TIAA Advice & Planning Services’ (“APS”) Portfolio Advisor Wrap Fee Disclosure Brochure. The ADV is a public disclosure document required by the Securities and Exchange Commission (SEC) of all professional investment advisors. The Form ADV discusses investment strategy, fee arrangements and service offerings. In my opinion, the relevant items are:

Compensation arrangements. In the “Advisor Compensation” portion of the ADV, TIAA states several times that “The compensation does not differ based on the underlying investments chosen within the solution, nor does the Advisor receive any client commissions or product fees.” While true, these “salaried” advisors do in fact earn “credits” towards their annual variable bonuses based on a number of factors. The ADV states clearly, “the annual variable bonus gives Advisors a financial incentive to enroll and retain client assets in the program” (i.e. a managed fee account, more complex solutions, or other TIAA products such as life insurance). The ADV states again that “Advisors have an incentive to and are compensated for enrolling and retaining client assets in TIAA accounts, products and services, but do not receive any client commissions or product fees.” Advisors are also compensated for “gathering, retaining, and consolidating” any new TIAA client accounts that they persuade clients to transfer to TIAA from other brokers (e.g. Morgan Stanley, Fidelity, Merrill Lynch, etc.).

In addition to the base salary received by all advisors, TIAA provides additional compensation in the form of variable annual bonuses to individual advisors. These bonuses are determined not only as a percentage of the amount of assets under management advisors accumulate, but also by the amount of wealth advisors are able to transfer from existing funds into their TIAA managed brokerage accounts. This means, that, while advisors receive a base salary (“no client commissions or product fees”), the bonus structure heavily influences advisors to move client assets to new managed accounts with added management fees, and to sell complex solutions (i.e., TIAA annuities or TIAA insurance) to their clients. In my opinion, this adds a conflict of interest similar to that of conventional brokers who receive higher commissions for selling certain products or certain funds. Yet, TIAA continues to emphasize its “no client commissions or product fees” mantra.

My additional concern about TIAA is that their recent more aggressive sales tactics seek to funnel existing TIAA clients nearing retirement into much higher cost TIAA Advice & Planning Services Advisor managed accounts. Enrolling in these accounts could result in retirees unknowingly paying additional fees to the advisor on top of the mutual fund fees they now pay in their current TIAA accounts. Accepting a TIAA Advisor’s Advice & Planning Services proposal contract includes substantial additional fees which may not be apparent to a customer who does not mine the depths of the lengthy ADV, Part 2 disclosure document.

How much would an unsuspecting TIAA client who converted to a TIAA Advisor wrap fee account pay annually? The TIAA fee schedule for Advisor & Planning services accounts is an asset-based program fee. (reproduced below from the Form ADV):

If a TIAA client with $500,000 in assets chose to work with a TIAA Advice & Planning Services advisor in a program account, their annual fees (in addition to annual mutual fund fees) would be $4,925; for a client with $1,000,000 in investments accounts, their annual fees would be $8,925. My concern is that TIAA clients contacted by or directed to a local TIAA advisor may not understand or realize the higher fees that come with that advisor’s proposals.

A final concern deals with TIAA directing existing clients to their local representative for a “review”, as we personally experienced. That “review” comes with a hidden incentive for the local representative to propose an advisor managed account. In addition to our being contacted by phone several times, the TIAA website has been redesigned to feature a prominent “My Advisor” icon on every page in the upper right. Existing clients who login to view their accounts and use that icon are directed to call their local TIAA representative. Why is the local representative “My Advisor” rather than TIAA representatives reachable by phone whom we have dealt with in the past?

TIAA has an exemplary not-for-profit heritage of serving education professionals with low cost, well-rated funds. While the TIAA Board of Overseers continues their service to nonprofit employers, the new TIAA Advice & Planning services business structure follows a more common brokerage firm model. Specifically, the way their advisors are compensated appears to incentivize TIAA salaried employees to steer clients to higher cost managed accounts and other insurance products and to gather additional assets held outside TIAA. I believe that this managed account model introduces a conflict of interest for advisors to serve the best interests of TIAA clients. Per the TIAA whistleblower’s complaint, this bonus compensation structure pushes advisors to move clients into products “more costly to clients while adding little value”. While a TIAA advisor’s proposed investment portfolio may appear more diversified due to including a larger number of TIAA funds, the client’s original choices of fewer funds without the managed account fee may serve that client’s interests just as well at a much lower cost.

In addition, a TIAA advisor managed account provides solely investment advice. While tailored to your “goals”, I believe investment decisions should be made in the context of a comprehensive financial plan, not as an isolated component. Without incorporating tax planning, management of other risks and a detailed cashflow analysis, tailoring an investment portfolio to “your goals” can lead to unintended consequences, especially when making decisions about retirement income from a portfolio. As for financial planning advice, I recommend consulting a trained Certified Financial Planner™ professional who, as a fiduciary, is bound to act in your best interests. Why pay TIAA to manage your accounts when, for a similar fee, a fee-only planner can provide a financial plan that includes portfolio management in the context of a comprehensive plan?

While Bluestem Financial Advisors continues to enjoy a strong working relationship with TIAA through the SURS state retirement program, transparency is of the utmost importance to us, and we hope it is for you as well. Buyer beware: a proposed portfolio promoted to you by your local TIAA advisor may come with much higher ongoing expenses than just continuing to self-manage your original lower-cost TIAA mutual fund choices.

Data security has been a hot issue for some time, however, the latest security breach at Equifax has left nearly half of all Americans exposed. In the wake of this troubling incident, many of us are left with questions pondering the safety of our personal information, and even our identity.

How could this security breach have happened?

Unfortunately, the best information we have received from Equifax is that the breach was due to a “website vulnerability”. What exactly this means is anyone’s guess. The important issue now is for all of us to protect ourselves in the safest manner possible.

What can someone do with my personal information?

To name a few of the numerous and frightening possibilities, an identity thief can open a line of credit, take out a prescription, and obtain a driver’s license. The results of the above theft include a ruined credit score, altered medical history, and costly tickets that could lead to a warrant for your arrest. This may sound very doom and gloom, but it’s a good reminder to stay alert and vigilant on all fronts.

What are the odds my identity would be stolen?

The likelihood of becoming a victim of identity theft may not appear to be very high. However, according to a recent USA Today article, 2016 saw a record rate of identity theft - about 1 in every 16 U.S. adults were victims¹. With the sheer volume of data stolen in the recent breach, one can only expect this number to rise in the coming years. Unfortunately, it has increasingly become a question of not if, but when one may be affected by identity theft. Nevertheless, there are several actions available to keep your identity as safe as possible.

To begin, Equifax has offered one year of free credit monitoring service to all individuals, the details of which you can review here. There has been concern raised regarding your ability to pursue legal action against Equifax if you accept this service. In a 9/11/17 update from Equifax, they state that enrolling does not waive any rights to take legal action, and that language on the contrary has been removed from their Terms of Use. However, if you are uncomfortable enrolling with in Equifax’s credit monitoring, see our three trusted steps below. Then continue reading for our general security tips. For maximum protection and security, complete all steps as often as recommended.

First: Routinely check your credit reports and account activity

Second: Place a Fraud Alert on your credit reports

Third: Place a Credit Freeze on your credit reports

Contact information for the Credit Reporting Agencies

TransUnion

1-800-680-7289

Experian

1-888-397-3742

Equifax

1-888-766-0008

General Safety Tips

If you have been the victim of identity theft visit the Federal Trade Commission’s ID Theft website for thorough tips on how to respond.

___________________________________________________________

1 USA Today article by author Bob Sullivan and published on February 6, 2017. (https://www.usatoday.com/story/money/personalfinance/2017/02/06/identity-theft-hit-all-time-high-2016/97398548/).

This month marks passage of the first Illinois state budget in over two years. The biggest changes resulting from this budget are to the Illinois tax code. Effective July 6th of this year (and retroactive to July 1st), the individual income tax rate has been increased to 4.95% along with other modifications to corporate tax and lesser used tax credits. Details of this bill are still coming, but we do know that this bill also requires changes to the State University Retirement System (SURS) Plan.

Under SB 0042 – Fiscal Year 2018 Budget Implementation Act, SURS is directed to create a new Tier III plan. All new employees hired who first become participants of SURS after the effective date of this new plan will have the choice of this new Tier III plan, the current Tier II plans (Traditional or Portable), or the Self-Managed Plan (SMP). SURS needs to work out many of the details for this new Tier III plan and formally adopt the changes before implementation. Therefore, we do not know the effective date at this point.

Further, existing employees in Tier II will also have the option to opt into Tier III, but the choice would be irrevocable. If you are uncertain which Tier plan you are in, Tier I generally applies to participants enrolled in a SURS Portable or Traditional pension plan before January 1, 2011. Everyone employed after this date is generally Tier II. The new Tier III pension plan would not affect those in Tier I plans or those who chose the Self-Managed Plan (SMP).

The overall goal of this Tier III program is the creation of a hybrid plan – a cross between a defined benefit and defined contribution pension system. In other words, it acts like a mix between the features of the Traditional/Portable Plans and the SMP Plan. Under Tier I and Tier II, the Traditional & Portable Plans are considered Defined Benefit pension plans. In these plans, the employer assumes all of the investment risk. The retirement income that you will receive is determined by a formula that takes into consideration your earnings and length of service. The SMP Plan is a Defined Contribution plan. The employer contributes a pre-determined percentage of your earnings to the SMP plan on your behalf. Those funds are deposited into your account to be invested at your direction (self-directed). This means you are responsible for selecting and managing the investments now and into the future. Your future retirement income depends on the balance of your SMP account at retirement.

Under this newest hybrid Tier III plan, you would get a combination of the two plan features above, albeit with a lower benefit from each. As laid out in the budget bill, the main features of the two components of the Tier III plan are:

Tier III Defined-Benefit Portion would include a pension based on:

Tier III Defined-Contribution Portion would have the following provisions:

Another big change in the budget bill shifts responsibility for funding the SURS employer contributions from the State of Illinois to each university. While increasing university budget expenses, this change will have a smaller impact directly on employees in the SURS system than the new Tier III hybrid plan.

While Tier I participants are not affected by the SURS changes, there are more proposed bills in the pipeline that may affect all SURS pension plan participants. One bill currently under consideration aims to slash the SURS pension Cost-of-Living Adjustment (COLA). To avoid the diminishment of benefits rule, it would offer defined benefit pension plan members a choice to keep their current COLA, but lose all rights to future increase in pension benefits as their salary increases; OR take a reduced COLA in exchange for continued accrual of future pension benefits and lower employee contributions. In other words, you could keep the COLA but lose future accrual of a higher initial pension or take a reduced COLA for continued benefit accrual. Additionally, the proposed legislation appears to offer lump sum buyouts to entice current members out of the SURS defined benefit plans. However, this bill has not passed yet and it is too uncertain to make predictions.

In all cases, there are still many details left before decisions can be made. We know changes are coming for new employees. Existing employees under Tier II Traditional or Portable plans will likely face an irrevocable choice to stay in Tier II or move to the new Tier III hybrid plan. However, SURS needs to make final plans before any analysis can be done. We will continue to monitor and keep our clients informed when changes will affect them.

For more information on the legislation discussed in this post click here.

To view our previous blog post on SURS plan selection click here.

The following post is shared content from the Alliance of Comprehensive Planners.

Tax-focused financial planning is not just for the one percent. On the contrary taxes are the hub of the financial wheel with consequences to virtually all financial decisions. Under-planning and overpaying simply delays financial independence. So, why don’t more Americans engage in tax-focused financial planning?

The disconnect between financial planning and tax planning is costing American taxpayers dearly. Aside from the many who intentionally allow higher withholding throughout the year just to claim a sizeable refund in April, are those who overlook the tax implications of their retirement distributions, investment allocations, estate planning decisions or education savings. All have tax liabilities attached, either in the short or long term.

Accountants and tax preparers might identify those consequences in hindsight, when it’s too late to avoid tax penalties. And, financial advisors,who often simply state, “consult your tax advisor” are just washing their hands of the tax consequences of their advice, leaving it up their client to connect the dots. Indeed, it is this short-sighted, often rear view, of taxes as a once-a-year task, rather than a pervasive feature of financial life, that makes the tax-focused financial planner uniquely positioned to advise clients in all aspects of their financial lives.

“All aspects” is a hefty claim. Yet, tax-focused financial planners are informed not only by their clients’ financial profile, but also by the real context and implications of their advice. Cash flow and financial behaviors, the expectations for children and demands of aging parents, job security and income growth are as important as retirement planning, investment strategy and the tax consequences for the all-of-it. It’s holistic. It’s fiduciary based. And, it’s decidedly uncommon.

Focusing on history, is as bad as ignoring it, and tax preparation is often just that: passive and backward-looking. Tax planning is anticipatory, active and looks forward, sometimes even beyond the current year to future years.

Those knee-deep in regret over the tax return they’re filing in April, might reconsider their approach for 2017. With a tax-focused financial planner, planning for their 2017 tax return would already be underway.

To read more on the subject of tax-focused financial planning check out the Tax Alpha White Paper written by fellow ACP Advisors Jonathan Heller and Robert Walsh (edited by Bluestem’s very own Karen Folk and Jake Kuebler). For more information on the Alliance of Comprehensive Planners visit their website at www.acplanners.org.

Guest Blogger: This post was written by Eric Schaefer, a senior studying Financial Planning at the University of Illinois. Eric is working towards becoming a Certified Financial Planner. He serves as President of U of I’s Financial Planning Club and is currently an intern at Bluestem Financial Advisors, LLC.

One of the cornerstones of a financial plan is protecting against the unexpected. We often address this through purchasing adequate life insurance coverage, maintaining proper emergency reserves (“ready cash”) and developing a thoroughly diversified investment portfolio. However, many overlook planning for unexpected financial events, especially those that may be particularly unpleasing. One such topic is, have you and your family thought about what you would do in the event of an unexpected medical emergency?

Following up on the HIPPA authorization article featured in our Fall Newsletter (Click Here to Subscribe), we would like to elaborate a bit further on the importance of having a medical emergency plan by highlighting a few key actions items to consider:

1.) To ensure family can get updates on you during a medical emergency, make sure that your HIPPA privacy forms are filled out completely and with the necessary signatures. Parents, if you have an adult child or student away at school, make sure they complete and sign the HIPPA form as well. You may also want to complete clinic specific authorization forms at their campus medical facilities. This will ensure that no matter where they receive emergency treatment you will have the appropriate access to their records and care providers.

2.) Upon admittance to the hospital, if the patient is unconscious the staff will first look for an EMERGENCY CONTACT card in a purse or wallet and/or check for an “in case of emergency” (ICE) contact in their phone. Modern cell phones often allow ICE contacts that can be accessed while our phone is locked. Some add on applications can also digitally display a Medical ID card from the lock screen.

If you aren’t the best with technology that’s OK! This would be a great opportunity for your children to show you by setting up their own digital ID on their phone. It’s also not a bad way to kill two birds with one stone. Additional information on how to set up and where to find these applications is listed below.

In the event that you either do not have a smart phone or would prefer to use a more traditional method for confirming your identification, there are many websites with Medical ID card templates that you can print out. Those with chronic conditions, allergies, or who are fashion oriented may consider Medical Emergency ID jewelry. What better gift to get your significant other, son or daughter than a necklace with their blood type and YOUR name and phone number on it?

3.) The alternative to carrying Medical ID cards or filling out numerous forms at different healthcare facilities would be to have a medical power of attorney, also referred to as an advanced healthcare directive. This is the most effective of all the options mentioned and an essential item in your estate plan. These medical power of attorney documents are state specific, so you will want to be sure to fill out the appropriate version for where your child plans to spend the majority of their time. Not only will this compliment a comprehensive medical emergency plan, but it will also afford your children the opportunity to begin thinking about and discussing with you the importance of life planning and determining what is truly important to them.

Here at Bluestem we would like to encourage all of you to address your physical well-being with the same careful and considerate preparation as you do with your financial well-being. Hopefully you nor your family members will ever be in a situation where you must utilize any of the items mentioned above, but in the event that you are, we hope that this post will have helped you make the necessary arrangements.

Additional Resources:

The U.S. Department of Labor just released its long-awaited fiduciary rule. The new rule aims to protect consumers saving in retirement accounts by amending the definition of fiduciary. The rule, in the pipeline for several years, applies to IRA, 401k, 403b and other retirement accounts that fall under the Employee Retirement Income Security Act (ERISA). Advisers and Brokers giving advice on investments in retirement accounts will now be required to act in the client’s best interest, i.e. when they offer advice on investment products in retirement accounts they must provide impartial advice and avoid conflicts of interest. Prior to this, they were only required to sell “suitable” investments to clients. While the rule does make a gallant effort to protect consumers, it also gives many concessions to commission sales-focused advisers. The rule implementation timeline was extended to January 1, 2018 (causing many to argue this simply gives more time for large companies to fight the rule); the rule also allows brokers to continue to sell certain products as long as they enter into a legal contract with the consumer that, among other things, discloses any conflicts of interest. How many consumers will read and understand such contracts? The rule has received considerable opposition from large investment firms, mainly those in the industry who are heavily sales-focused. Their major complaints revolve around new compliance regulations and the fact that the rule will dramatically alter their former commission based-sales approach. The prior “suitability” rule has no requirement to put the consumer’s best interest above the advisor’s interests.

While many in the financial services industry are upset by the new rule, others, like Bluestem, welcome the new consumer protections and are thrilled that the DOL is making an effort to help protect individuals saving for retirement. As a Fiduciary, Registered Investment Advisor, Bluestem always has and always will put our client’s best interest first. We are proud to be a fee-only financial planning firm and will continue to offer unbiased advice and stellar service to all of our clients. While other firms need regulatory nudging to get on board with fiduciary standards, we live by them every day. In fact, the financial planning organizations we belong to, NAPFA and ACP, believe that the new rule is a step in the right direction to add much needed consumer protections.

So how does this DOL rule affect Bluestem? In a nutshell, it doesn’t. It’s very possible that there may be some new regulatory compliance procedures for us, but in the big picture, Bluestem isn’t making any changes. Bluestem is passionate about fee-only, no product sales, financial planning. It’s this passion for fee-only planning that has kept us on the right side of this issue from the beginning. While others will be clamoring to further water down the new rule or put up a fight to protect their outdated and biased way of offering “financial advice”, Bluestem will continue our efforts to provide trusted, clear-cut advice and spread the word about our professional fee-only alternative to product sales masquerading as financial planning.

For most of us, getting organized to complete our annual Income Tax Return is a chore. We would prefer to expend the minimum amount of effort to get the job done. Luckily, many records such as income figures are provided to us by others (W-2’s, 1099’s etc). In addition, minimizing your taxes due often involves documenting charitable gifts for itemized deductions. Maximizing the benefits from those charitable gifts does require a bit more work on your part.

While you may be aware that you need to keep records to deduct charitable gifts you make, you may not realize that it is fairly common not to receive IRS-compliant documentation from nonprofit organizations. Therefore, it is up to you to know the rules yourself and confirm you receive the correct documents. Below is an outline of what to keep when you make Charitable Gifts (by donating Cash, Check, via Credit Card, etc):

For Gifts under $250:

You need to have a record showing the name of the organization, date and amount of the contribution. One or the other of these will work:

us, getting organized to complete our annual Income Tax Return is a chore. We would prefer to expend the minimum amount of effort to get the job done. Luckily, many records such as income figures are provided to us by others (W-2’s, 1099’s etc). In addition, minimizing your taxes due often involves documenting charitable gifts for itemized deductions. Maximizing the benefits from those charitable gifts does require a bit more work on your part.

While you may be aware that you need to keep records to deduct charitable gifts you make, you may not realize that it is fairly common not to receive IRS-compliant documentation from nonprofit organizations. Therefore, it is up to you to know the rules yourself and confirm you receive the correct documents. Below is an outline of what to keep when you make Charitable Gifts (by donating Cash, Check, via Credit Card, etc):

For Gifts under $250:

You need to have a record showing the name of the organization, date and amount of the contribution. One or the other of these will work: